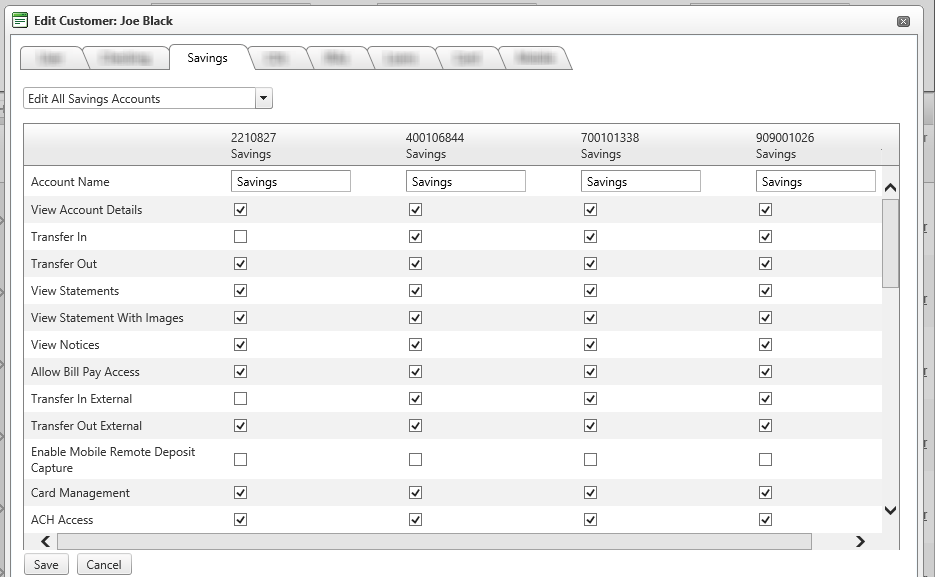

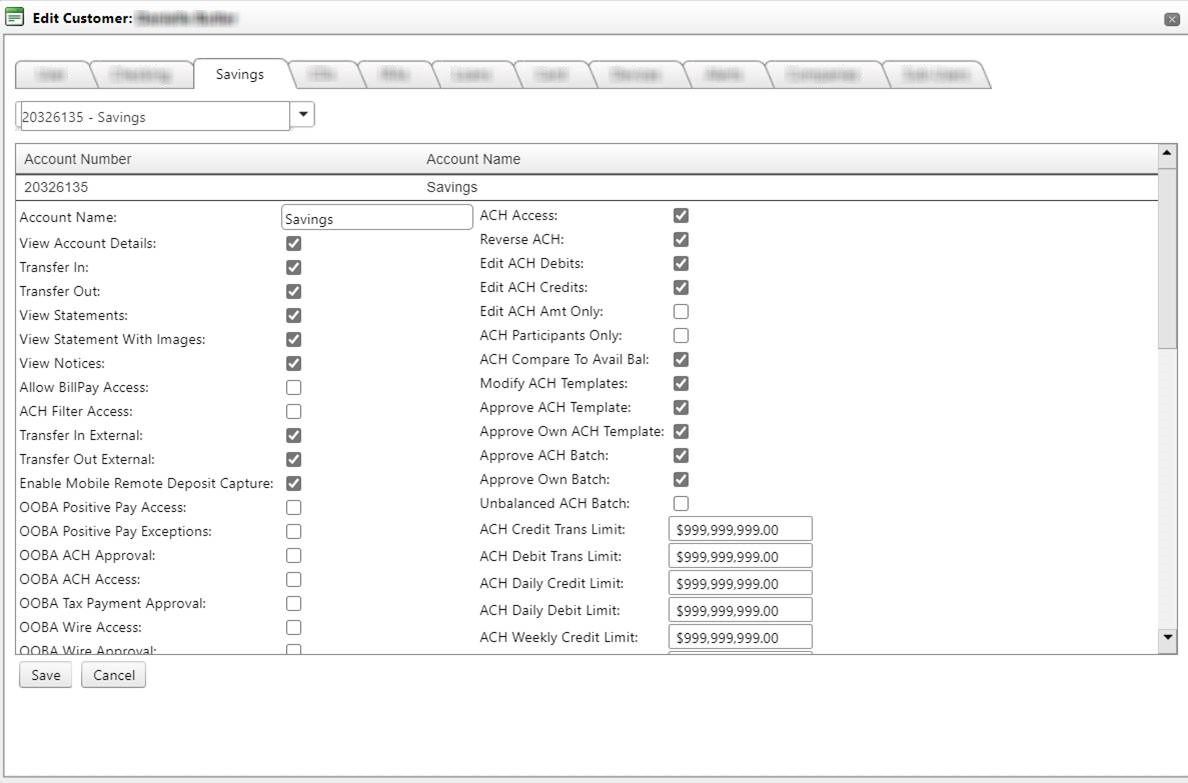

Edit Customer >> Savings tab

All Accounts

Account Detail

Left Column

- Account Name:

will reflect the name of the account; by default it will be reflective of the account application, but if changed by the user, the nickname of the account will display here. - View Account Details:

when enabled, the user will have the ability to view the account within digital banking, including its balances and transactional information. They will also be able to grant permission of this account to sub-users if sub-user functionality is offered. When this option is disabled by an admin user, customers are unable to see the account. For example, if the customer has just one savings account and an admin user un-checks the View Account Details box on the customer's checking account, the Savings tab will not be seen by the customer.

When this option is disabled, customers are also unable to transfer money out of the specific account. The Transfer Out and Transfer Out External options automatically become disabled upon saving for Checking and Savings accounts. For advancing loans, the Allow Advance option is disabled automatically upon save which means that those accounts cannot make advances. These options remain disabled until the user enables the View Account Details option for the account. Users are however, still able to transfer into these Checking and Savings accounts.

Note: The information pertaining to transfer to and from accounts, loan payments, and loan advances is dependent on the user having the necessary permissions to perform the transfers, payments, and advances.

Since accounts with the "View Account Details" option disabled are unable to transfer out, they do not appear in the "From Account" drop down menu but do appear in the "To Account" drop down menu under the Transfers tab. When transferring to an account with the option disabled, the account will not display a balance in the transfer confirmation screens since the user does not have permission to view account details.

Since accounts with the "View Account Details" option disabled are unable to transfer out, they do not appear in the "From Account" drop down menu under the Loan Payment tab but loans with the option disabled are displayed in the Loan drop down menu. When making a payment to a loan with the option disabled, the loan will not display a balance in the payment confirmation screens since the user does not have permission to view account details.

Since accounts with the "View Account Details" option disabled are unable to transfer out, they do not appear in the "Loan" drop down menu under the Loan Advances tab but loans with the Checking and Savings accounts with the option disabled are displayed in the To Account drop down menu. When making an advance to a Checking or Savings account with the option disabled, the account will not display a balance in the loan advance confirmation screens since the user does not have permission to view account details.

When making a Quick Transfer, each of the other Checking and Savings accounts are listed but balances only appear for accounts that have the option enabled; this applies to the Quick Transfer tab and the confirmation screens for the transfers.

If you try to make a quick transfer from one of the accounts with the option disabled, they will receive a message letting them know that they do not have permission to transfer from the account and the transfer will not go through.

When making a Quick Payment, the only accounts listed to make a payment from are the accounts with the option enabled.

If an account has ACH and/or Wire permissions enabled, they will be able to use the account regardless of the "View Account Details" option status.

If an account has the "View Account Details" option disabled, they will not be able to grant access to that account to any of their sub users. Accounts that have the option disabled will not be displayed in the "Grant Access To:" drop down menu located on the Settings > Sub-users tab.

- Transfer In: allow inbound transfers from an internal account

- Transfer Out: allow outbound transfers to an internal account

- View Statements: allow statements to be visible

- View Statement With Images: allow statements to be visible with images

- View Notices: when enabled, this allows notices to be visible

- Allow Bill Pay Access: when enabled, the customer will have bill pay access and can pay from the account

- ACH Filter Access:

- Transfer In External: When marked, gives customers the ability to make a transfer from an external account into an internal Checking or Savings account. This field is only visible when External Transfers are enabled.

- Transfer Out External: When marked, gives customers the ability to make a transfer from an internal Checking or Savings account to an external account. This field is only visible when External Transfers are enabled.

- Enable Remote Deposit Capture: when enabled, this feature allows a customer to make a deposit, via mobile app, to the account

- OOBA Positive Pay Exceptions: Not selected by default. With this box checked, when the customer logs in and goes to the Positive Pay Exceptions tab, the Requires OOBA window appears. If the customer has the device set up as a mobile that can receive text messages, they have the option to receive a mobile app push, phone call, or passcode.

- OOBA Positive Pay Access: invalid

- OOBA ACH Approval: Not selected by default. With this box checked, when the customer logs in and approves an ACH batch, the Requires OOBA window appears. If the customer has the device set up as a mobile that can receive text messages, they have the option to receive a mobile app push, phone call, or passcode.

- OOBA ACH Access: invalid

- OOBA Tax Payment Approval: Not selected by default. With this box checked, when the customer logs in and approves an ACH Tax Payment, the Requires OOBA window appears. If the customer has the device set up as a mobile that can receive text messages, they have the option to receive a mobile app push, phone call, or passcode.

- OOBA Wire Approval: Not selected by default. With this box checked, when the customer logs in and goes to the Wire Approval tab, the Requires OOBA window appears. If the customer has the device set up as a mobile that can receive text messages, they have the option to receive a mobile app push, phone call, or passcode.

- OOBA Wire Access: invalid

- OOBA Access Cash Management: Not selected by default. With the Access Cash Management box checked, when the customer logs in and goes to the Cash Manger tab, the Requires OOBA window appears. If the customer has the device set up as a mobile that can receive text messages, they have the option to receive a mobile app push, phone call, or passcode.

- OOBA External Transfers: Not selected by default. With this box checked, when the customer logs in and goes submits an External Transfer, the Requires OOBA window appears. If the customer has the device set up as a mobile that can receive text messages, they have the option to receive a mobile app push, phone call, or passcode.

- OOBA Bill Pay Access: Not selected by default. With this box checked, if the customer is Enrolled in bill pay and has the Warn if Leaving Main Site Via Bill Pay Link flag checked, then the Requires OOBA window will appear. If the customer has the device set up as a mobile that can receive text messages, they have the option to receive a mobile app push, phone call, or passcode.

- OOBA Sub User Save: Not selected by default. With this box checked, when the customer logs in and makes changes to a checking account, the Requires OOBA window appears. If the customer has the device set up as a mobile that can receive text messages, they have the option to receive a mobile app push, phone call, or passcode. Note: This applies to the sub-user’s permissions for checking accounts only. You are able to grant permissions to CDs, IRAs, and external accounts without OOBA. Sub-users are also able to be added and deleted without authentication.

- OOBA iPay Payment Scheduling: Not selected by default. With this box checked, when the customer schedules an iPay bill payment, the requires OOBA window appears. If the customer has the device setup as a mobile that can receive text messages, they have the option to receive a mobile app push, phone call, or passcode.

- OOBA Remote Deposit Capture: With this option enabled, customers will be prompted to verify their identity via device when selecting the RDC tab under Cash Management. If the customer has the device set up as a mobile that can receive text messages, they have the option to receive a mobile app push, phone call, or passcode.

- OOBA Card PIN Change: with this option enabled, customers will be required to authenticate themselves before a PIN change can be completed. If the customer has the device set up as a mobile that can receive text messages, they have the option to receive a mobile app push, phone call, or passcode.

- OOBA Card Limit Suspension: with this option enabled, customers will be required to authenticate themselves before the limit suspension feature can be completed. If the customer has the device set up as a mobile that can receive text messages, they have the option to receive a mobile app push, phone call, or passcode.

- Authenticator Positive Pay Exceptions: Not selected by default. With this box checked, when the customer logs in and goes to the Positive Pay Exceptions tab, authentication via token will be required. Based on authentication method (token or mobile app) the system will require response.

- Authenticator Positive Pay Access: invalid

- Authenticator ACH Approval: Not selected by default .With this box checked, when the customer logs in and approves an ACH batch, the requires authentication window appears. Based on authentication method (token or mobile app) the system will require response.

- Authentication ACH Access: invalid

- Authenticator Tax Payment Approval: Not selected by default. With this box checked, when the customer logs in and approves an ACH Tax Payment, the requires authentication window appears Based on authentication method (token or mobile app) the system will require response.

- Authentication Wire Approval: Not selected by default. With this box checked, when the customer logs in and goes to the Wire Approval tab, the requires authentication window appears. Based on the authentication method (token or mobile app) the system will require response

- Authentication Wire Access: invalid

- Authentication Access Cash Management: Not selected by default. With the Access Cash Management box checked, when the customer logs in and goes to the Cash Manger tab, the requires authentication window appears. Based on the authentication method (token or mobile app) the system will require response.

- Authentication External Transfers: Not selected by default. With this box checked, when the customer logs in and goes submits an External Transfer, the requires authentication window appears. Based on authentication method (token or mobile app) the system will require response

- Authentication Bill Pay Access: Not selected by default. With this box checked, if the customer is Enrolled in bill pay and has the Warn if Leaving Main Site Via Bill Pay Link flag checked, then the requires authentication window appears. Based on authentication method (token or mobile app) the system will require response.

- Authentication Sub User Save: Not selected by default. With this box checked, when the customer logs in and makes changes to a checking account, the requires authentication window appears.. Based on the authentication method (token or mobile app) the system will require response. Note: This applies to the sub-user’s permissions for checking accounts only. You are able to grant permissions to CDs, IRAs, and external accounts without Authentication. Sub-users are also able to be added and deleted without authentication.

- Authentication iPay Payment Scheduling: Not selected by default. With this box checked, when the customer schedules an iPay bill payment, the requires authentication window appears. Based on authentication method (token or mobile app) the system will require response.

- Authentication Remote Deposit Capture: With this option enabled, customers will be prompted to verify their identity via token or mobile app when selecting the RDC tab under Cash Management. Based on authentication method (token or mobile app) the system will require response.

- Authentication Card PIN Change: with this option enabled, customers will be required to authenticate themselves before a PIN change can be completed. Based on authentication method (token or mobile app) the system will require response.

- OOBA Card Limit Suspension: with this option enabled, customers will be required to authenticate themselves before the limit suspension feature can be completed. Based on authentication method (token or mobile app) the system will require response.

Right Column

60027

|

Customer Portal

Customer Portal